On 17 January 2023, the European Parliament approved a revised version of the draft Anti-Tax Avoidance Directive (ATAD 3), known as the Unshell Directive.

The Unshell Directive, first published in December 2021, aims to combat the misuse of shell entities across EU member states.

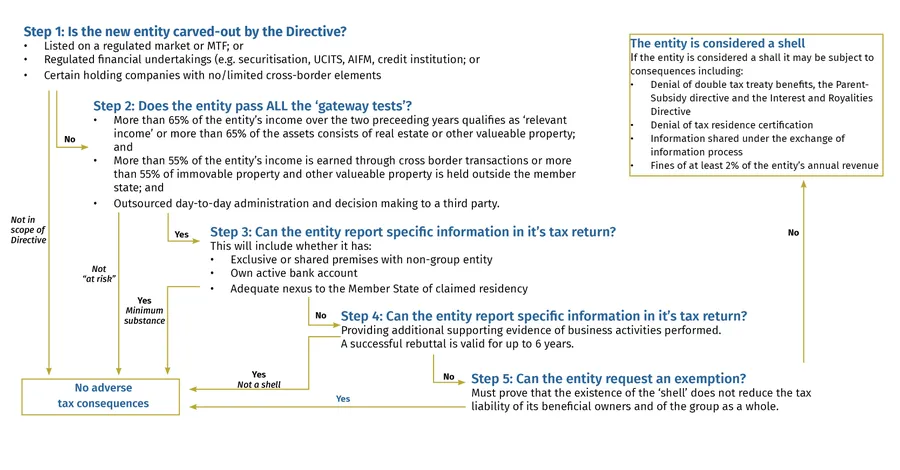

Under the Unshell Directive, qualifying entities which do not meet minimum substance requirements would be subject to additional reporting obligations and a variety of tax penalties. The proposed penalties for non-compliance range from denial of tax treaty benefits to financial penalties of at least 2% of the entity’s annual revenue.

The decision tree below summarises the steps in determining how the Unshell Directive could impact an entity’s operations.

It was originally intended by the European Commission that by January 2024, the Directive would enter into force. It was also planned that by this point the automatic exchange of information on reporting entities would be established, with the central directory for administrative cooperation operational by June 2024.

If adopted, the Unshell Directive would need to be transposed into the national legislation of all EU member states by 30 June 2023, and would be effective from 1 January 2024. However, given the two-year lookback period in assessing whether economic substance, the directive would in effect apply retroactively from 1 January 2022.

The European Parliament has rebuffed attempts to push back the enforcement date to 2025. In any case, given the ongoing negotiations at the Council of the European Union (including the lookback period and implementation), the effective date of the Unshell directive may yet be postponed.

In terms of next steps, the amendments approved by the European Parliament will now be considered by the Council of the European Union. The Council is not bound to accept the changes. The final text will require the unanimous support of the representative of all member states.

The Unshell Directive has the potential to significantly impact a wide variety of entities including holding companies, certain section 110 vehicles, funding vehicles, leasing entities and entities which are part of a multinational group. It is important for organisations to carefully assess their current structures and holdings to assess their exposure.